Book Value Greater Than Salvage Value

:max_bytes(150000):strip_icc()/BalanceSheet-32ba95b3f8454cd8b923cd5e9a942cae.jpg)

Book Value Vs Salvage Value What S The Difference

How Are Book Value And Market Value Different

Interactive Notebook Place Value Includes 12 Activities Covering Topics Expanded Form Word Fo Interactive Notebooks Math Interactive Notebook Place Values

Irr Formula Google Meklesana Formula Math Cash Flow

Pin On Hope

Pin On God S Word

Salvage value or scrap value is the estimated value of an asset after its useful life is over and therefore cannot be used for its original purpose.

Book value greater than salvage value. It is possible to get the price per book value by dividing the market price of a company s shares by its book value per share. In depreciation the residual value is the estimated scrap or salvage value at the end of the asset s useful life. Intangible assets are excluded from a company s liquidation value.

At the end of its useful life the net book value of an asset should approximately equal its salvage value. For example if the machinery of a company has a life of 5 years and at the end of 5 years its value is only 5000 then 5000 is the salvage value. Calculatingdepreciation when salvage value exceeds net book value nbv there are instances when the residual value salvagevalue of an asset may increase to an amount equal to or greater thanthe asset s carrying amount nbv.

Impairment is a situation where the market value of an asset is less than its net book value in which case the accountant writes down the remaining net book value of the asset to its market value. By comparing an asset s book value cost less accumulated depreciation with its selling price or net amount realized if there are selling expenses the company may show either a gain or loss. Net book value from above 1 338 750 at the end of five years salvage value 1 600 000 sale price of asset at the end of five years gain salvage nbv 261 250 taxable gain on disposal gains tax 35 profit 91 438 the tax treament of capital gains may apply here this is one assumption that can be used net proceeds gain tax 169 813 that is capital gains are taxed at ordinary income rates it.

The book value of a company is the amount of owner s or stockholders equity. Note that the book value of the asset can never dip below the salvage value even if the calculated expense that year is large enough to put it below this value. To arrive at the book value simply subtract the depreciation to date from the cost.

The liquidation value is the value of a company s real estate fixtures equipment and inventory. Liquidation value is usually. The book value of an asset is the amount of cost in its asset account less the accumulated depreciation applicable to the asset.

Accounting For Not For Profit Organisation Cbse Notes For Class 12 Accountancy Learn Cbse Learn Accounting Accounting Accounting Notes

Quiz Worksheet Solving Graphing One Variable Inequalities Graphing Inequalities Solving Inequalities Graphing Worksheets

Episodic Soap Note Tom Walker Nrp 531 Latest 2020 Complete In 2020 Soap Note Tom Walker Soap

Pin On Tina S Church Ideas

Thank You Lord Jesus Praise God Faith Quotes Inspirational Quotes

Hope Dances In The Puddles Til The Sun Comes Out Again E Cards Wonderful Words Inspirational Words

Net Book Value Overview Formula And Importance

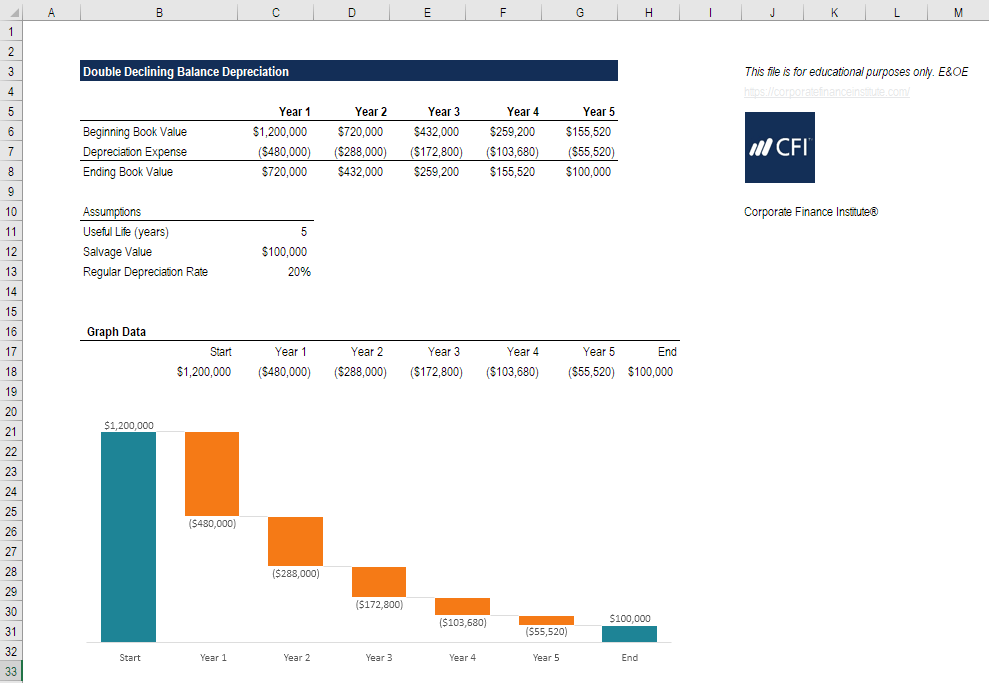

Double Declining Balance Depreciation Examples Guide

God Is At Work Transforming People And Nations Through Business Ken Eldred David Yonggi Cho 9780984091102 Ama Eldred Christian Business Business Practices

The Perks Of Being A Wallflower Framed Quote This Movie Makes Me Realize What Life S About Perks Of Being A Wallflower Quotes Wallflower Quotes Quotes

How To Get Through Those Bad Mom Days Electric Mommy Blog Bad Mom Parenting Mom Mom Care

Pin On Gifted

Motivation By Faith Motivationbyfaith Instagram Photos And Videos Faith Quotes Faith Motivation