Book Value Of Equipment Is Computed By Taking

How To Calculate Book Value 13 Steps With Pictures Wikihow

Book Value Of Assets Definition Formula Calculation With Examples

Book Value Per Share Equity Ratio Analysis Ch 15 P 8 Intermediate Accounting Cpa Exam Cpa Exam Equity Ratio Book Value

How To Calculate The Book Value Per Share Price To Book P B Ratio Using Market Capitalization Youtube

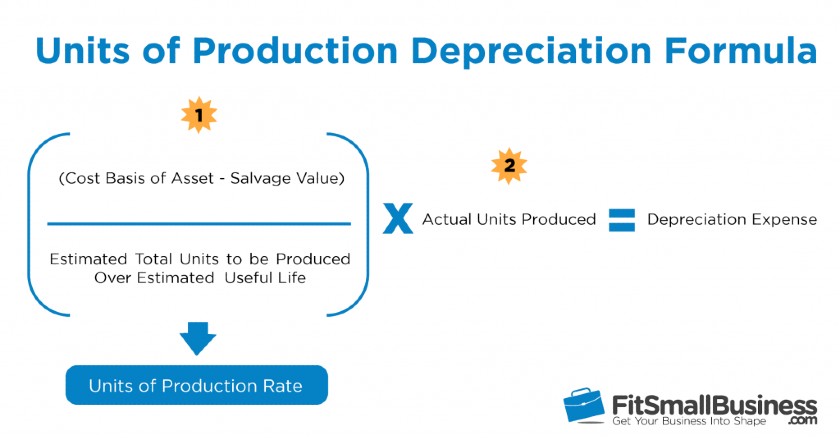

Units Of Production Depreciation How To Calculate Formula

Pin On Ct Scan

It can be useful to compare the market price of shares to the book value.

Book value of equipment is computed by taking. How to calculate book value the book value formula the calculation of book value includes the following factors. Depreciable assets have lasting value and they include items such as furniture equipment buildings and other personal property. For assets the value is based on the original cost of the asset less any depreciation amortization or impairment costs made against the asset.

Book value does not need to be calculated for more stable assets that aren t subject to depreciation such as cash and land. A company s asset book value can be an annual or quarterly accounting record. To make this easier convert total book value to book value per share.

Original purchase price subsequent additional expenditures charged to the item accumulated depreciation impairment charges book value. Example of book value. Divide 35 million by 1 4 million shares for a book value per share of 25.

Therefore the calculation of book value per share will be as follows bvps total common shareholders equity preferred stock number of outstanding common shares 2 93 491 00 cr 592 18 cr. It is calculated by taking the total value of the company s assets minus its intangible assets and liabilities. You can use this book value calculator.

Book value per share will be bvps 495 61 book value calculator. Equipment values equipment category attachments auctions services buildings barns real estate chemical applicators construction equipment grain handling and storage harvesting hay forage lawn and garden livestock manure feeders miscellaneous planting equipment precision ag equipment software recreational utility rotary cutters and shredders skid steer loader loaders tillage tires wheels tracks. For example a piece of manufacturing equipment was purchased for 10 000 and depreciation over 4 years totaled 4 000.

Nbv is calculated using the asset s original cost how much it cost to acquire the asset with the depreciation depletion or amortization of the asset being subtracted from the asset s original cost. Market value is the price a willing buyer would pay a willing seller. Suppose a company has a book value of 35 million and there are 1 4 million common shares outstanding.

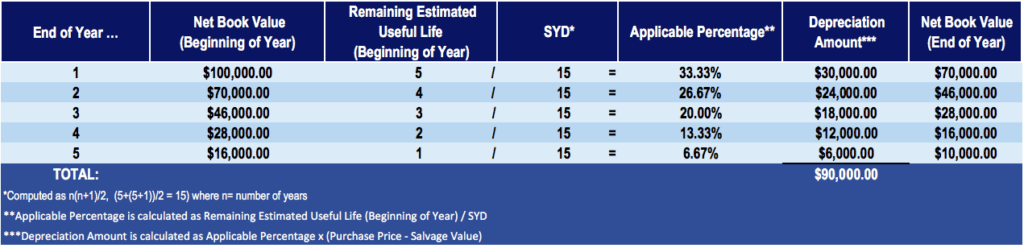

Accelerated Depreciation Overviews Examples Methods

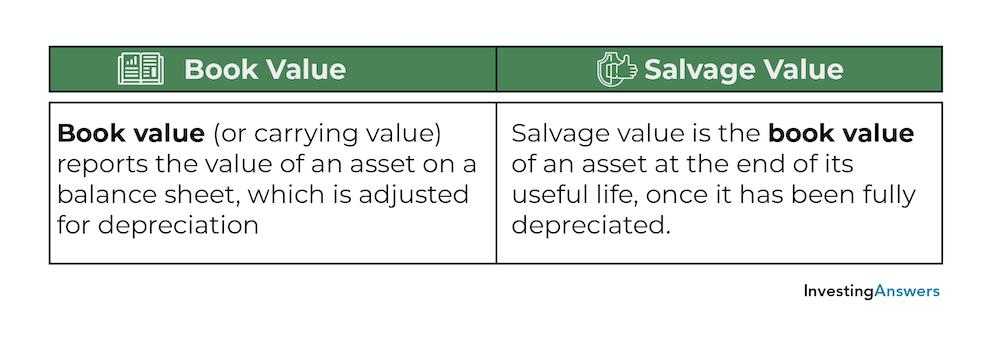

Book Value Definition Example Investinganswers

Do You Know How 3d Printing Works In 2020 What Is 3d Printing 3d Printing Materials Printer Types

Magnetic Resonance Imaging Mri You Need To Know What Is Mri In 2020 Mri Magnetic Resonance Imaging Magnetic Resonance

Fahrenheit 451 Dutch Translation Agreement Ray Bradbury Signed Contract Book Publishing

/dotdash_Final_Property_Plant_and_Equipment_PPE_Sep_2020-01-dd61e2f2fdb7481d81e95bc90b5c61d8.jpg)

Property Plant And Equipment Pp E Definition

Action Words For Resumes Resumes Ideas Another Great List To Start Polishing Up A Resume I Tailo Resume Action Words Resume Power Words Resume Words

Depreciation Definition Life Is Good Method Life

Ct Scanner Tomography Pet Scanner For Pet Full Body Tomography Discovery Iq Ge Healthcare Medical Device Design Medical Design Healthcare Design

Images Of Computed Tomography Google Search Medical Design Medical Equipment College Life

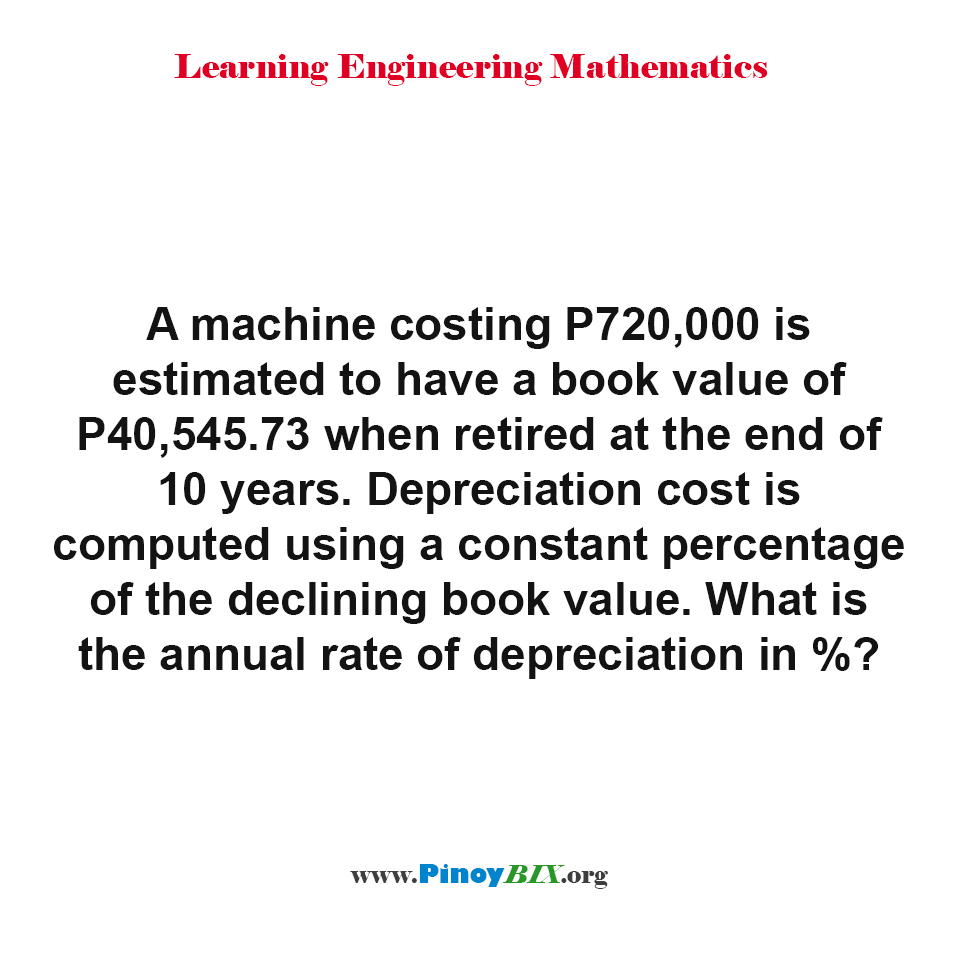

Solution What Is The Annual Rate Of Depreciation Of The Machine In Percentage

Pin On Brain Functions

Podobny Obraz Resume Action Words Resume Power Words Resume Words