Book Value Per Share Minority Interest

Book Value Of Equity Per Share Bvps Definition

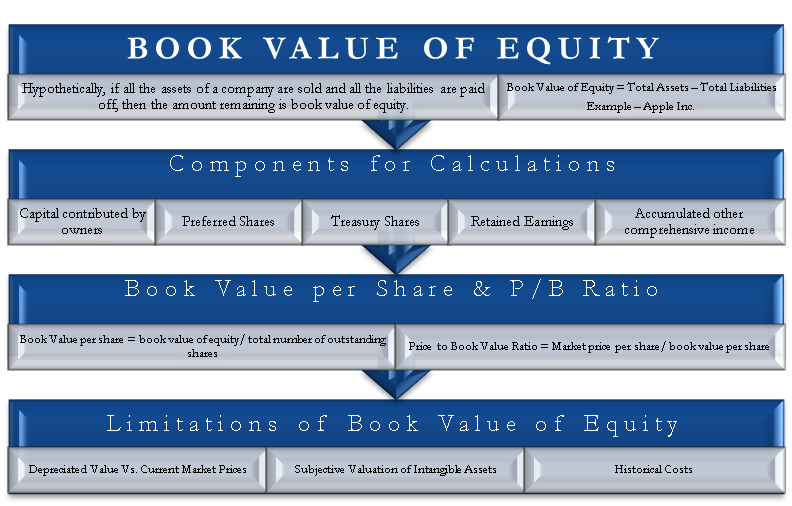

Book Value Of Equity Meaning Formula Calculation Limitation P B Ratio

Understanding Non Controlling Interests Ncis Financial Edge Training

Minority Interest Meaning Valuation How To Account

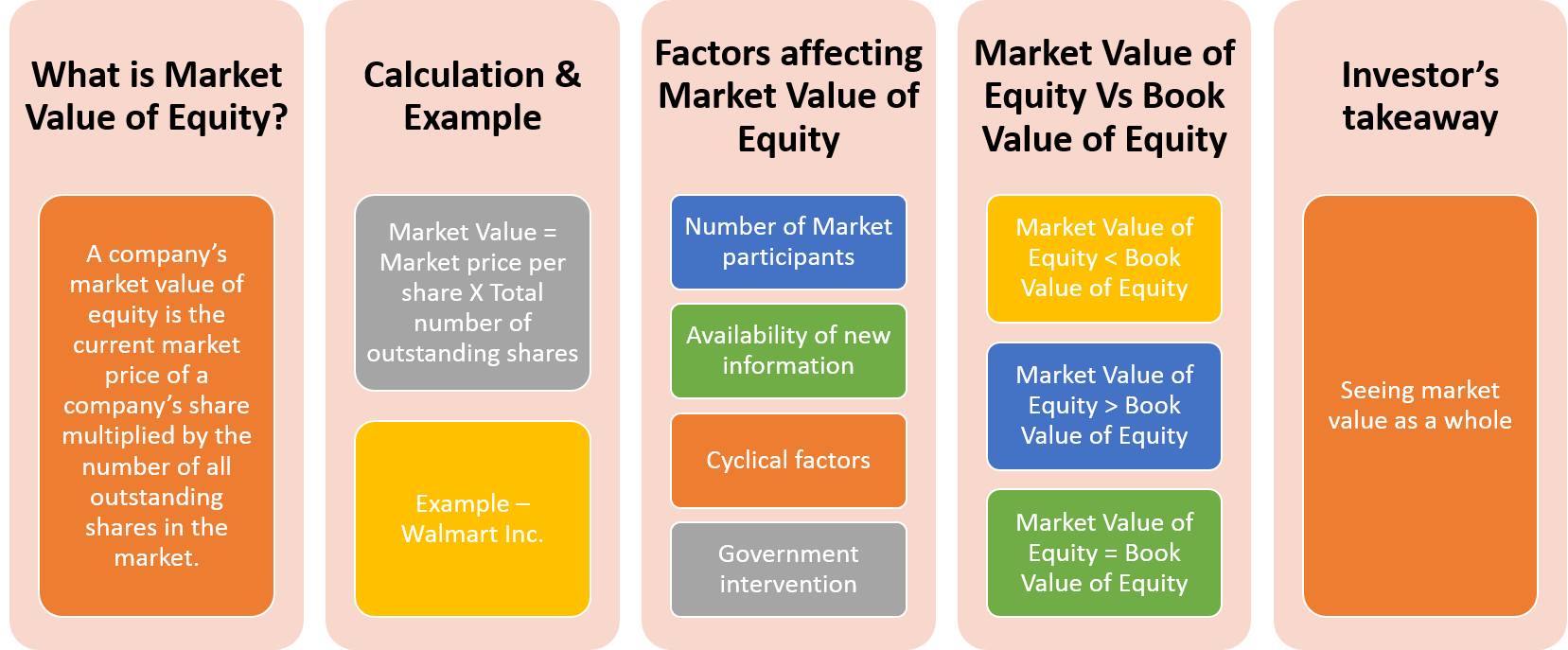

Market Value Of Equity Calculate Example Factors Vs Book Value Efm

Https Samples Breakingintowallstreet Com S3 Amazonaws Com Ibig 04 04 Equity Value Enterprise Value Metrics Multiples Pdf

Kinder morgan kmi which had a total of 10 billion in minority interest liability removed from shareholder value in 2012.

Book value per share minority interest. When a company owns more than 50 but less than 100 of a subsidiary they record all 100 of that company s revenue costs and other income statement items even. In simple words minority interest is the value of a share or the interest attributable to the shareholders holding less than 50 of the total number of shares. The term book value is a company s assets minus its liabilities and is sometimes referred to as stockholder s equity owner s equity shareholder s equity or simply equity.

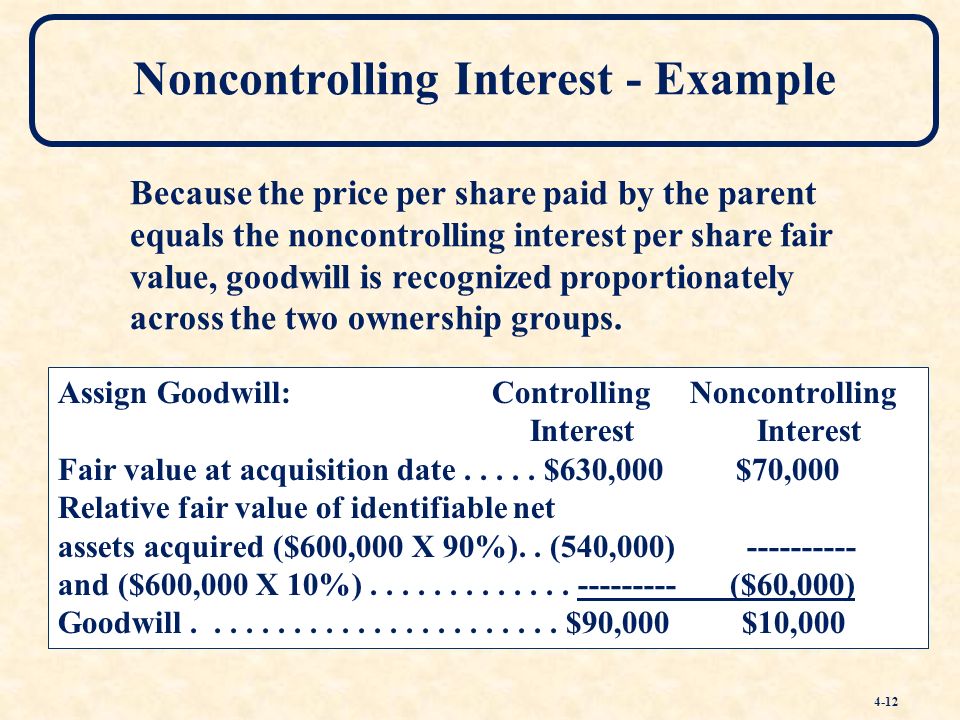

We then multiply this book value by 100 90 10 which is the percentage of pcp owned by minority shareholders to arrive at the minority interest value of 55 2 million to be reported on. Shareholders holding less than 50 of the total outstanding number of shares are known as minority shareholders. Learn more about how to calculate this ratio what it tells you and how investors use it to guide their decisions.

It is also known as non controlling interest. The book value per share formula is used to calculate the per share value of a company based on its equity available to common shareholders. The correct value is lower.

Book value per share is a way to measure the net asset value. Next multiply that book value by the percentage. In other words this measures a company s total assets minus its total liabilities on a per share basis.

The parent paid 40 000 more than book value for its 80 percent interest. To calculate a parent company s interest share in a subsidiary the first step is the find the book value of that subsidiary on its balance sheet. Proponents of using book values of the subsidiary s net assets view consolidated financial statements from the parent s viewpoint.

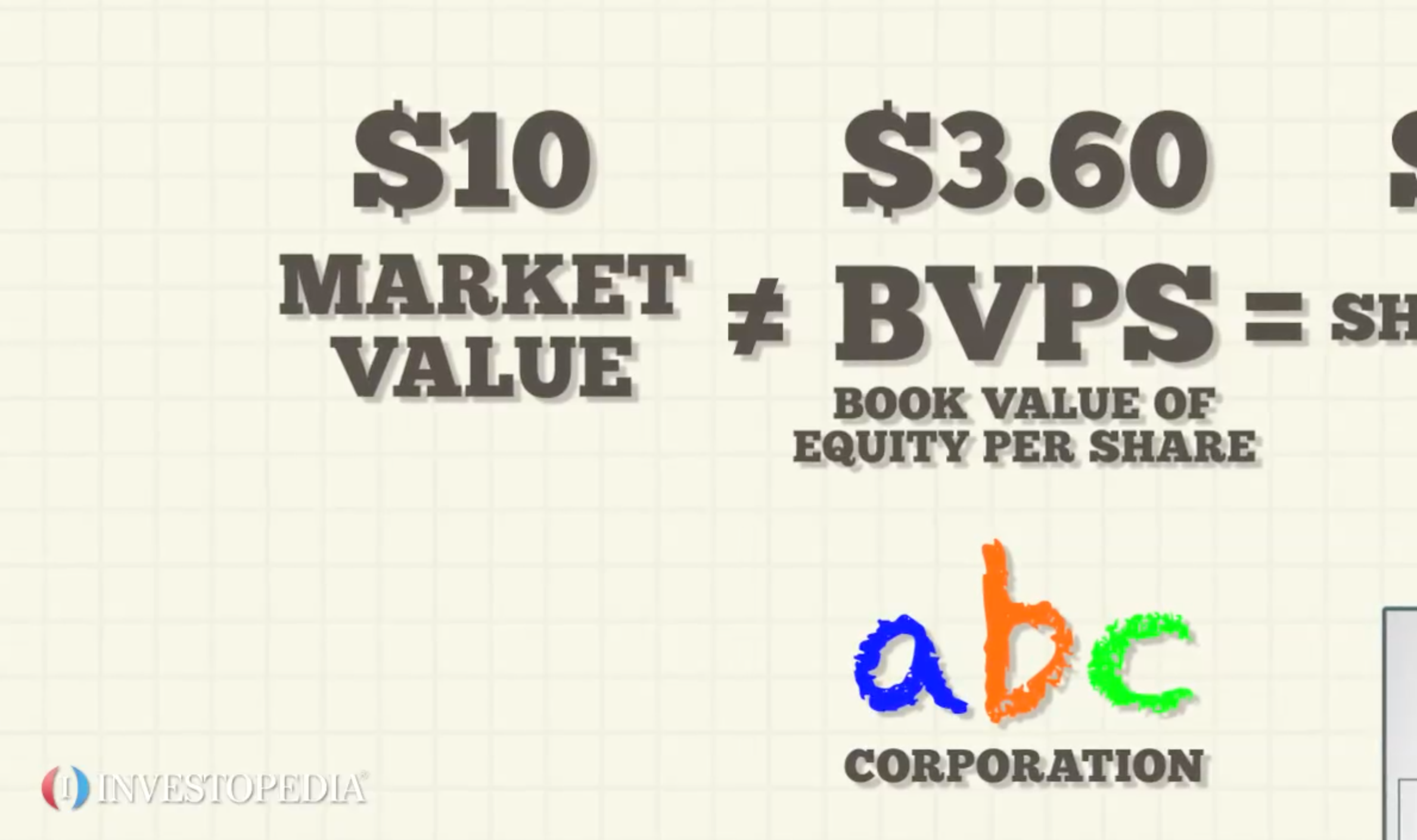

The book value per share bvps is a ratio that weighs stockholders total equity against the number of shares outstanding. This adjustment lowered kmi s economic book value from 1 6 billion to 8 6 billion. Enterprise value has to be adjusted by adding minority interest to account for consolidated reporting on the income statement.

Introduction To Levels Of Value In Business Valuation Chris Mercer

Enterprise Value Ev Formula Definition And Examples Of Ev

Consolidated Financial Statements And Outside Ownership Ppt Download

Diluted Earnings Per Share Diluted Eps Explained Financial Edge Training

:max_bytes(150000):strip_icc()/GettyImages-10188160-d7657047525045728e3d437c8cb592f1.jpg)

Book Value Vs Market Value What S The Difference

/stocks-lrg-2-5bfc2b1d46e0fb0051bdcc6a.jpg)

Digging Into Book Value

Roic Formula Examples How To Calculate Roic

Apple Pb Ratio Aapl Gurufocus Com

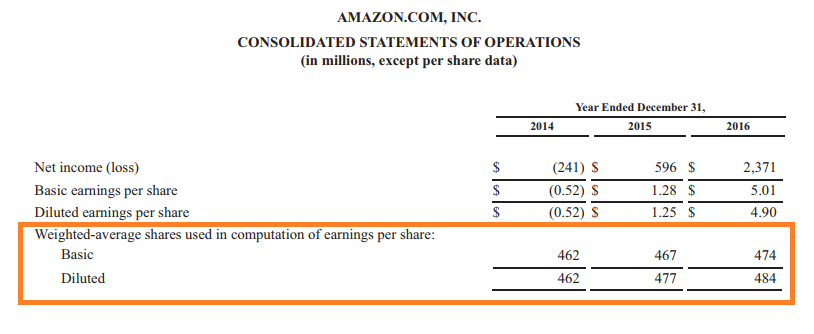

Weighted Average Shares Outstanding Example How To Calculate

:max_bytes(150000):strip_icc()/dotdash_Final_Equity_Aug_2020-01-b0851dc05b9c4748a4a8284e8e926ba5.jpg)

Equity Definition

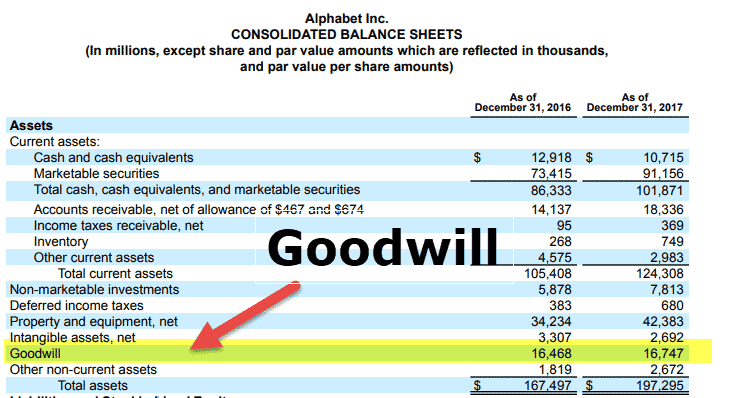

Goodwill In Accounting Definition Example How To Calculate

How To Calculate Minority Interest In Consolidated Balance Sheet Video Tutorial In Hindi In 2020 Accounting Education Learn Accounting Videos Tutorial

Doc Final Requirement In Advacc Michelle Pisala Academia Edu