Depreciation Net Book Value Formula

Net Book Value Meaning Formula Calculate Net Book Value

Net Book Value Youtube

Ad Glossary Net Book Value

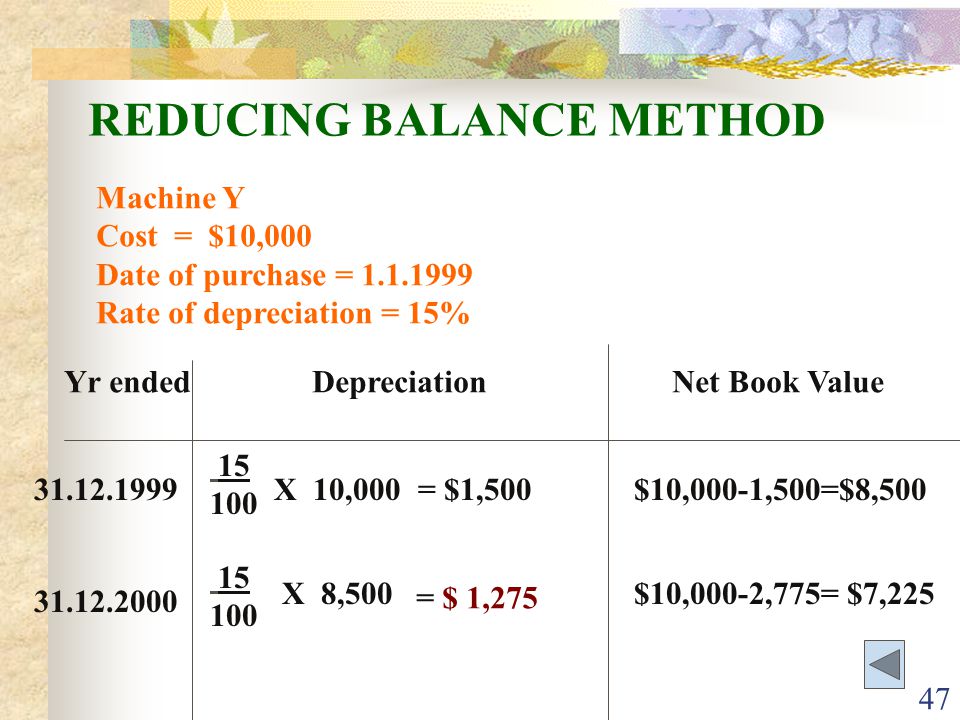

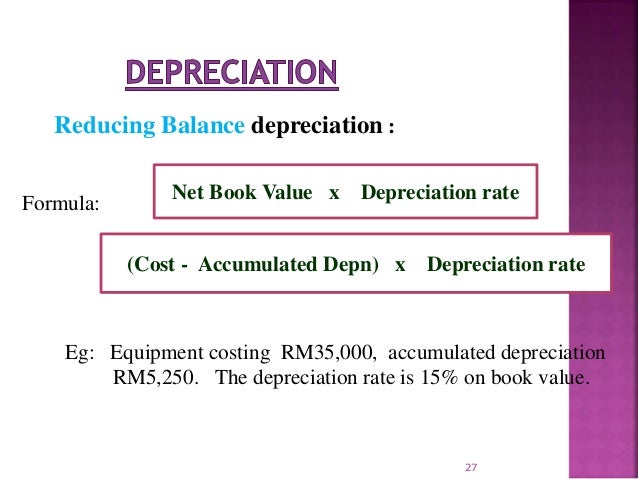

Reducing Balance Depreciation Calculation Double Entry Bookkeeping

Depreciation Ppt Video Online Download

Topic5 Compthe Acccycle Robiah

Book value of assets formula.

Depreciation net book value formula. The vehicle is worth 34 000 at the end of year one. Calculating net book value. In year two depreciation is 5 100 34 000 x 15 percent and in year three depreciation is 4 335 28 900 x 15 percent.

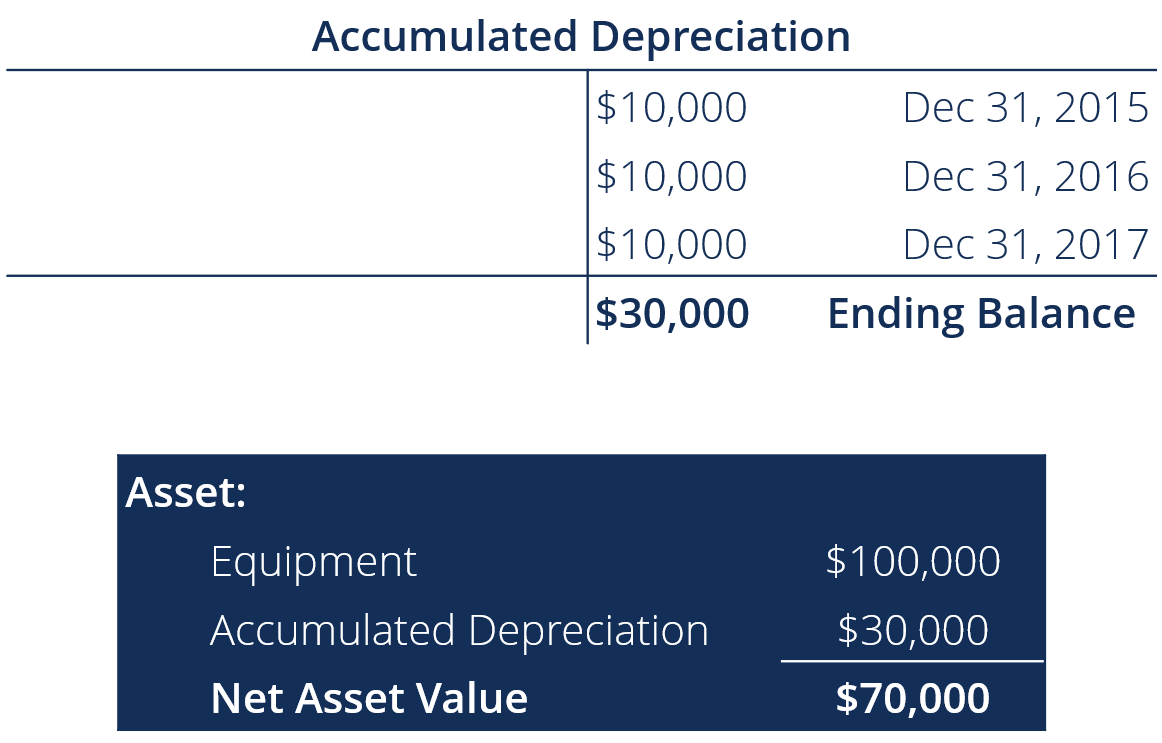

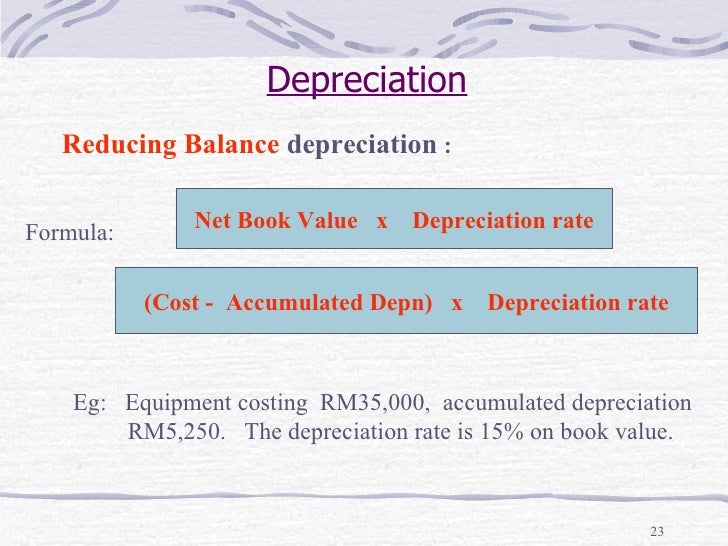

Other cost include impairment cost and related costs. Accumulated depreciation per year depreciation x total number of years. Note how the book value of the machine at the end of year 5 is the same as the salvage value.

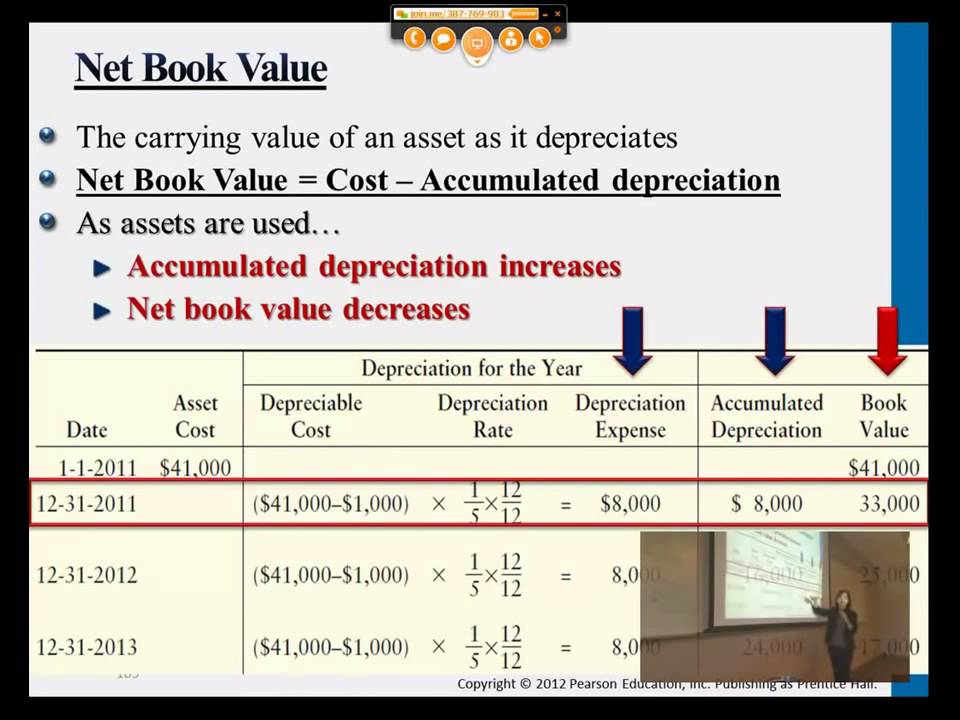

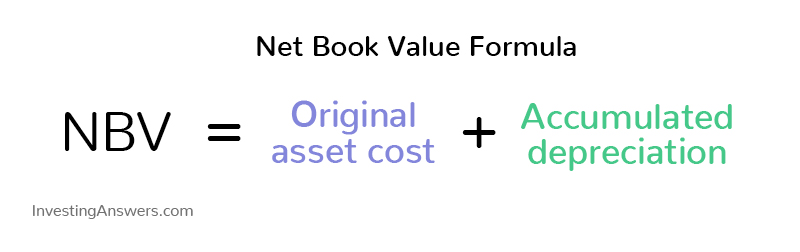

Net book value original asset cost accumulated depreciation. When it reaches the end of its useful life the nbv should be equal to its salvage value. The net book value of an asset is calculated by deducting the depreciation and amortization of an asset from its original cost.

Depreciation 2 straight line depreciation percent book value at the beginning of the accounting period. Total value of the asset value at which the asset is purchased. In this case the machine has a straight line depreciation rate of 16 000 80 000 20.

The depreciation rate is the annual depreciation amount total depreciable cost. As the name suggests it counts expense twice as much as the book value of the asset every year. Formula for net book value net book value cost of the asset accumulated depreciation.

The formula for calculating nbv is as follows. Under the straight line depreciation method the company would deduct 2 700 per year for 10 years that is 30 000 minus 3 000 divided by 10. The original cost of an asset includes the original cost of acquisition plus any costs associated with the delivery and intended use of an asset to the purchase price.

Straight Line Depreciation Formula Guide To Calculate Depreciation

Net Book Value Nbv Definition Meaning Investinganswers

How To Calculate Book Value 13 Steps With Pictures Wikihow

Straight Line Depreciation Method Definition Formula Example Graph Journal Entries Advantages And Disadvantages

Carrying Value Definition Formula How To Calculate Carrying Value

Carrying Amount Definition Formula How To Calculate

Depreciation Formula Financial Accounting Book Value Straight Lines

Declining Balance Depreciation Double Entry Bookkeeping

Written Down Value Method Of Depreciation Calculation

Akaun Chapter 4

Net Book Value Of Fixed Assets Wikiaccounting

Reducing Balance Depreciation Calculator Double Entry Bookkeeping

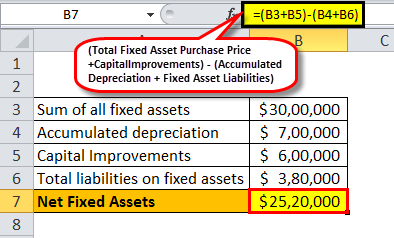

Net Fixed Assets Formula Examples How To Calculate